Scoping out dates and mates by their credit scores at first seems far fetched and overblown. Not to mention it pretty much kills romance. CNN reported on credit scores and dating. My colleague Frank Pipitone took off on the idea. But there is a kernel of wisdom there that couples in California need to heed. […]

Creditor Must Pay If It Loses A Bankruptcy Fight

The game isn’t very fair when the players are mismatched. Though bankruptcy court is hardly a game, it’s been unfair when it comes to attorneys fees for the winning party. California law provides that when a contract allows one party their fees if they prevail, the other party got their fees if they won. So, […]

Your Home Loan May Be Excluded From Homeowner Bill of Rights

Homeowners whose loans were originally made by a federally chartered savings bank are excluded from protections of HBOR, a federal judge has ruled. Dual tracking is back on the rails California Homeowners Bill of Rights, enacted January, 2013, prohibited dual tracking of mortgages: that is, the lender could not simultaneously consider a loan modification and prosecute […]

Your Creditors Lie In Wait For Your Kids

Is your legacy to your kids an encounter with your unpaid creditors? Debt problems for those over 65 may not be problems for the elder at all. Income and assets are largely protected by law from creditors. But that doesn’t trouble creditors: they’ll simply wait and get their money from your kids. Seniors enjoy protection […]

The Killer Rule That Zaps Private Student Loans

Got private student loans? I’ve got good news and bad news. Bad news first. Private Student Loans Inflexible Private student loans have no built in mechanisms for deferment and forbearances, like government-backed loans do. There are no income based repayment plans, as there are with federal student loans.’ No “outs” for disability or schools that close […]

Foreclosure: The Unseen Hazards

It’s not the foreclosing creditor that really threaten California homeowners. It’s the forces that follow foreclosure. The junior lender and the tax man can deliver truly punishing blows to a family losing a home. Cut-off Junior Lienholders Californians enjoy the protection of the one action rule governing foreclosures. A creditor who conducts a non judicial […]

Bank Has No Remedy After Foreclosure

Facing foreclosure is bad enough; worrying about your exposure afterwards is worse. Breathe deeply. California laws shield homeowners from further collection by a lender who has foreclosed. Understanding Foreclosure Sales To understand California’s protections for homeowners, you have to understand how a typical foreclosure sale works. The deed of trust, given to the lender when […]

Earthquake In California Law Of Community Property And Title

The ground has shifted under California real property law. The change looms as large as a quake along the San Andreas fault that runs through our neighborhood. The words on a real property deed no longer mean exactly what they say when the property owners are married to each other. The newly decided Brace case holds that the […]

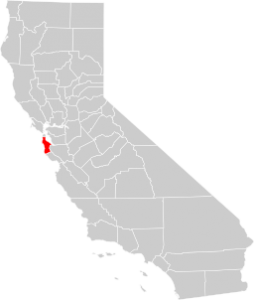

Can You Afford The Cost of Retiring Here In California?

Care to guess what it will cost a retired couple in San Mateo County to meet their basic living needs? If they rent, it takes $3193 a month. If they have a mortgage, it rises to $4247. Those dollars cover housing, food, medical, transportation and $376 for everything else. Social security doesn’t cut it The average Social […]

Free Expert Help With Your Bay Area Home Loan Modification

Applying for a mortgage modification is equal parts torture and miracle drug. It can mean the difference between staying in your home and foreclosure. Yet it comes with more questions than answers. What’s the difference between HAMP and HARP? Do I want to appear broke or prosperous? Should I default before I apply? Critical questions, the […]

- « Previous Page

- 1

- …

- 5

- 6

- 7

- 8

- Next Page »